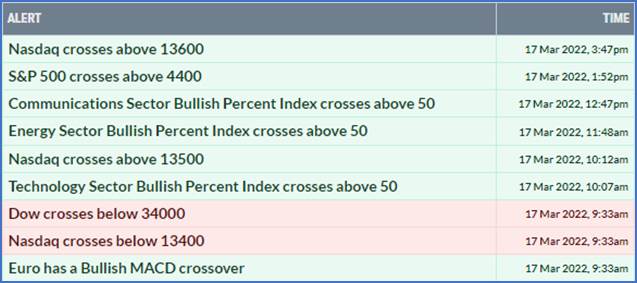

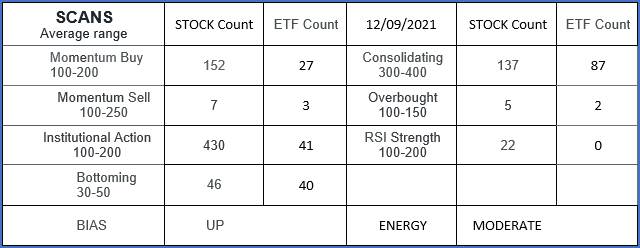

Market Update Examples

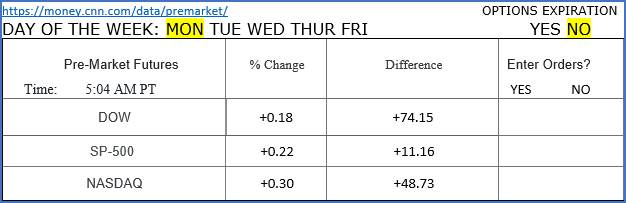

MARCH 18 – FRIDAY MARKET COMMENTS

Dark Pools were accumulating deeply discounted stocks below company fundamentals. HFTs followed gapping many stocks which activated VWAP orders. Total volume was lower. Sellers disappeared. Equities are up against resistance.

Russian default risks drops with JPM and C collecting and distributing $117 million in interest payment. The West’s sanctions will be negative for Russia, but it is not “cut off” from the global economy with many large countries are not following the U.S.’s lead.

The Kremlin casts doubts on peace talk with Ukraine, and energy prices are back above $100. Volatility in high beta, energy and metals market isn’t gone but may moderate with signs of resolution. The geopolitical risks will moderate but resolution in Ukraine is likely months away. The threat of nuclear attack will be a psychological tool if the Ukrainians persist in a strong or at least persistent defense. Russian military continues striking civilian targets. If Putin seems to be losing, chemicals and nuclear may become more than threats. Constantly repeating that the West won’t intervene raises the probability.

Biden will try convincing Xi Jinping to pressure Putin to end his war. If not, he will threaten to “impose costs” on China for supporting Russia. However, since Hunter Biden’s laptop has been certified and revealed the cash for policy changes, Xi Jinping likely knows what is unknown to us that can embarrass Biden as an offset to any “costs.”

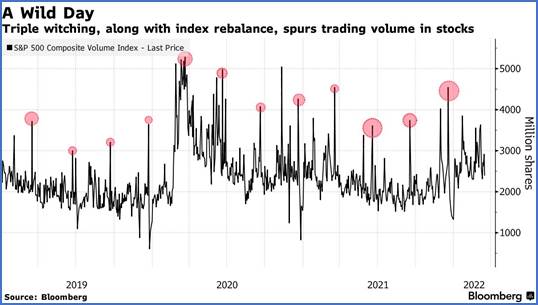

Today is triple witching day. Approximately $3.5 trillion of stock options expire today.

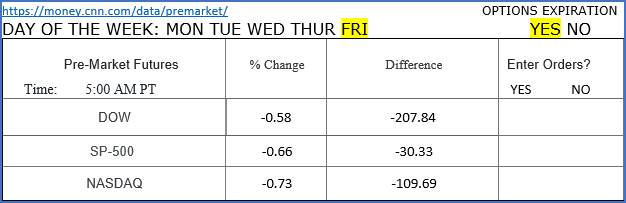

While stocks rose over the past few days, Ukraine and threatening stagflation are causing concerns this morning. Overnight, Asian markets were higher except in Hong Kong where tech fears rose again. U.S. futures slipped, with those on the S&P 500 and Nasdaq 100 both down about 0.6%. In Europe, autos and energy were the worst performing sectors. Oil pared some gains but was still up on the day. The dollar was higher. Gold and Bitcoin fell. GS position is that market risks are being underestimated.

5 minute candles at 8:45 AM EST. The red line is Thursday’s close.

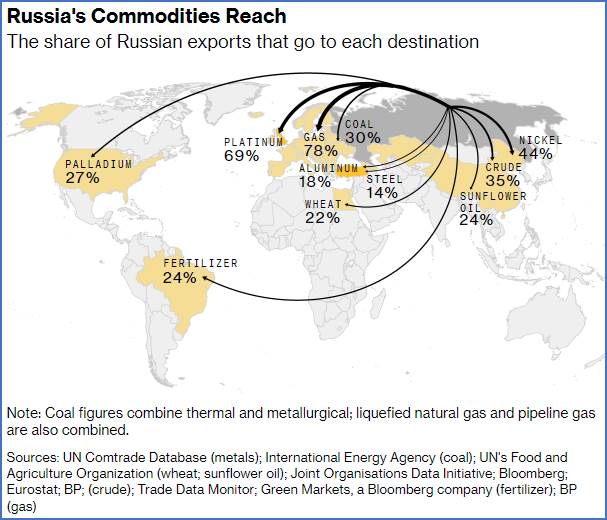

Beyond oil and gas, the war is causing prices of commodities to rise. Capitalizing on significant discounts, the third largest energy consumer, India, bought Russian oil that was rejected by Western buyers.

Monetary policy is not science but theory and an uncertain “tool” to manage the economy. A recession may not be needed but the Fed is just guessing about what is needed to arrest inflation. The answer probably requires lower asset prices. Higher interest rates are expected with the Fed’s analysis that the economy is strong enough to adapt to flattening yield curve. Investors should be concerned that the Fed could be making a policy error. Since 1945, the Fed has had 17 hiking cycles with the S&P rising on average 1.3% within 6 months.

The 10-year rate is now lower than the five. Other comparisons are close to inverting but the 5-10 is a recession warning.

Prior to the Russian invasion of Ukraine, hiking interest rates were to be a benefit for the banking industry. The war changed investors’ opinion and decisions which have led to an exit from many bank industry ETFs. Outflows have impacted XLF, BNK, KBWB, EUFN and others with gold and Treasury based ETFs being the beneficiaries.

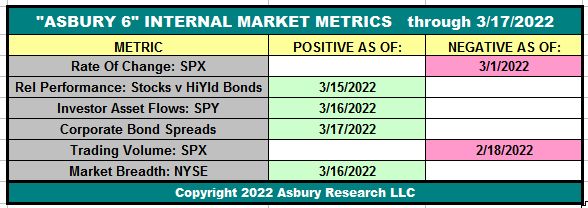

Recent trading has generated significant shift is risk indicators in my charts as well as in Asbury’s.

Heee’s back. Fauci surfaced yesterday joining Pfizer’s warning that booster #4 is required to deal with a coming rise in Covid cases.

After earning $53 million in two years, the CEO of Lyme Timber says “buying carbon offsets” isn’t working as a means of “saving the planet.”

After earning record profits trading commodities, traders are pressed for cash and want a central bank bailout as provided Wall Street after 2008.

AAPL has a new process for buying the iPhone bypassing major carriers and retail outlets. Activate the phone and pay Apple directly.

GE hasn’t met growth targets. CEO Culp’s compensation is cut in half.

The U.S.A. weather forecast is for an extension of minor to severe drought conditions being the largest drought condition since 2013. A lack of rain and snow is impacting the West Coast to the Lower Mississippi Valley.

Flow of Funds Report for week ending Wednesday March 16th.

Conventional Equity Funds outflows of 3.1 billion

Conventional Bond Funds outflows of 3.8 billion

ETF Funds outflows of 6.3 billion

ETF Bonds outflows of 6.1 billion

Money Market Funds outflows of 19 billion

Crypto Currencies outflows of 6 billion.

MARCH 28 – MONDAY MARKET COMMENTS

Friday’s volume was below average though the broader base of stocks are beginning to break upward from trading ranges. Dark Pools continue accumulating in stocks that are not brand name companies. As earning season begins in next few weeks, the major banks and energy companies should have higher earnings. Last quarter, CEOs were conservative with estimates leaving low benchmarks to provide positive earnings reports.

After ignoring all the data in 2021, the Fed is now data dependent regarding the need for a 0.50% rate hike, or perhaps it’ll only be 0.25%. Is that called planning ahead?

The war is causing shortages of palladium and price hikes for steel, aluminum and nickel posing real problems for the auto industry. S&P Global Ratings has reduced 2022 expected auto sales by 2% with a greater impact in Europe.

Will they never learn? What you tax you get less of. Consider the demographic migration in our country of people and businesses leaving high tax states for lower tax states. The Administration is proposing a minimum 20% tax on incomes and unrealized gains on assets of the “wealthiest” households. Every EU country that did this reversed the tax decision which was a failure. Apparently, the Administration knows how to make it work. Those affected households can afford to move to a tax haven country.

Overnight, European stocks are brushing off a downbeat Asia session. S&P futures reversed early losses to trade higher. Bonds slid from Australia to the U.S., with the TNX yield trading at 2.5%. The 5-30 part of the Treasury curve inverted for the first time since 2006. The Japanese yen weakened to trade above 125 per dollar – a move last seen in August 2015. Crude futures dropped over $4 with WTI stalling near $109. Spot gold slumped to $1,926.

5-minute candles at 8:45 AM EDT. Red line is Friday’s close.

The SPX recaptured its 200-SMA (4,477) last week along with resistance off the September highs at 4,537. The next major hurdle for the index is at 4,589 (Feb highs) then 4,634 (mid-Dec low). Momentum indicators remain bullish with limited signs of overbought conditions. Breadth is improving with around half of the index trading above their 200-SMAs. There is mounting technical evidence that the correction lows are in.

Inflation is beginning to take a toll on global demand with food, fuel, plastics and metals prices rising above what many households can afford. Consumer slow down is impacting trucking with prices and volume dropping. Perhaps these factors are why the Fed expects to see 2% inflation near year’s end, but it would be a change in seasonal patterns.

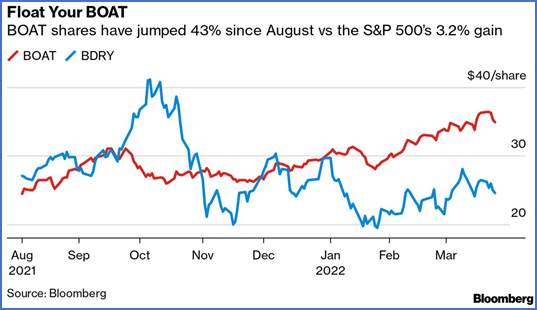

ETF BOAT was launched last August tracking fifty stocks of container handling companies, dry-bulk carriers and tankers. Gains in the industry are expected with global realignment due to geopolitical and economic changes alter company dominance.

Russian oil exports are much larger than we ever gave a second thought to until the war. However, as the second largest global exporter of crude oil. It is the third largest producer behind the U.S.A. and Saudi Arabia. The impact and duration of sanctions is disrupting global supplies remains unknown. Bond payments and interest are taken for granted until now with sanctions leaving fund managers uncertain and attorneys concerned about violating sanctions if they intervene to obtain payments.

XLE rose 7.6% last week and broke out from a bullish pennant formation. Above the rising 50-/200-SMAs. RSI has moved higher off the midline and MACD had a buy signal. A close above the ’18 highs ($79) should open the door to another leg higher.

XOP cleared resistance ($124) from the ‘19 highs. It is above the rising 50-/200-SMAs. RSI and MACD confirm the breakout. The next levels of resistance are near $148 and $164 (‘18 highs).

The Administration’s hope for Iranian oil to mitigate prices is in doubt as Tehran makes new demands.

The war has accelerated a shift away from King Dollar. A debate about currency dominance is underway similar to the post-WWII debate.

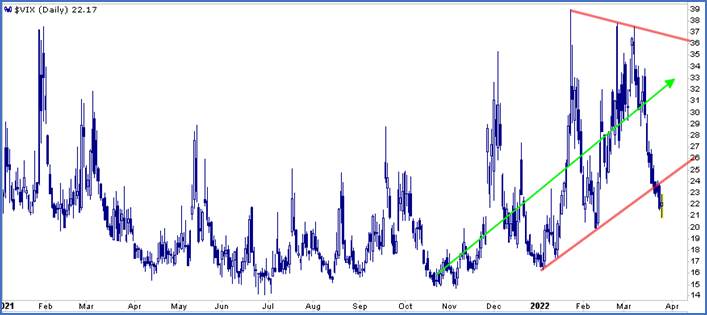

Trading in the ETNs – VXX and OIL – were suspended last week as the sponsor, Barclay’s Bank, quit issuing new shares and withdrew support of the ETNs. The bank rescinded and refunded shares in excess of authorized registration. Nevertheless, the VIX-X is improving trading conditions as it has lower highs and broke through a rising trendline. An upward bias persists but has not been scaring investors away from equities.

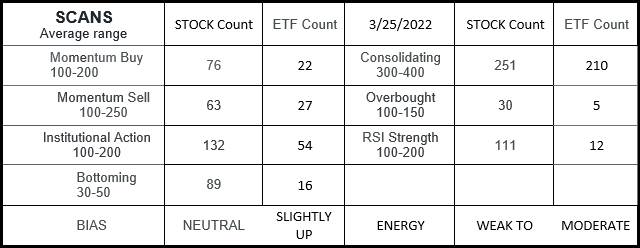

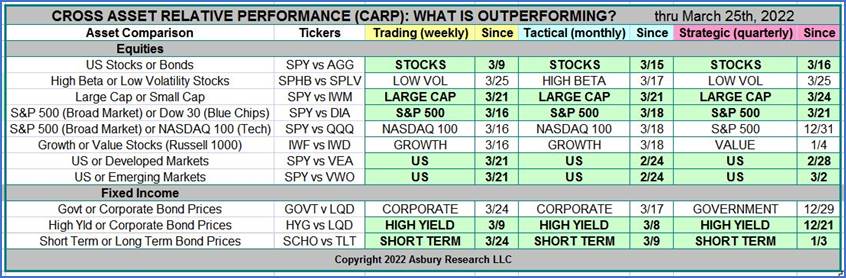

Within a trading range, high beta and low volatility have swapped leadership again as seen in the above table and here:

A new mutation of omicron is wide spread in China, U.K. and now in the U.S.A. An emergency authorization application was submitted by Moderna for a booster for children. Not everyone is on board.